My investment in Franklin India Prima Fund continues in the sixth year. Along with the fund house renaming it from Franklin India Prima Fund and me stopping my SIP in Jan’25 there were no other significant events that happened since last one year. I plan to continue to hold this fund for long term and will restart my SIPs once my current financial commitments are taken care of.

Figure 1

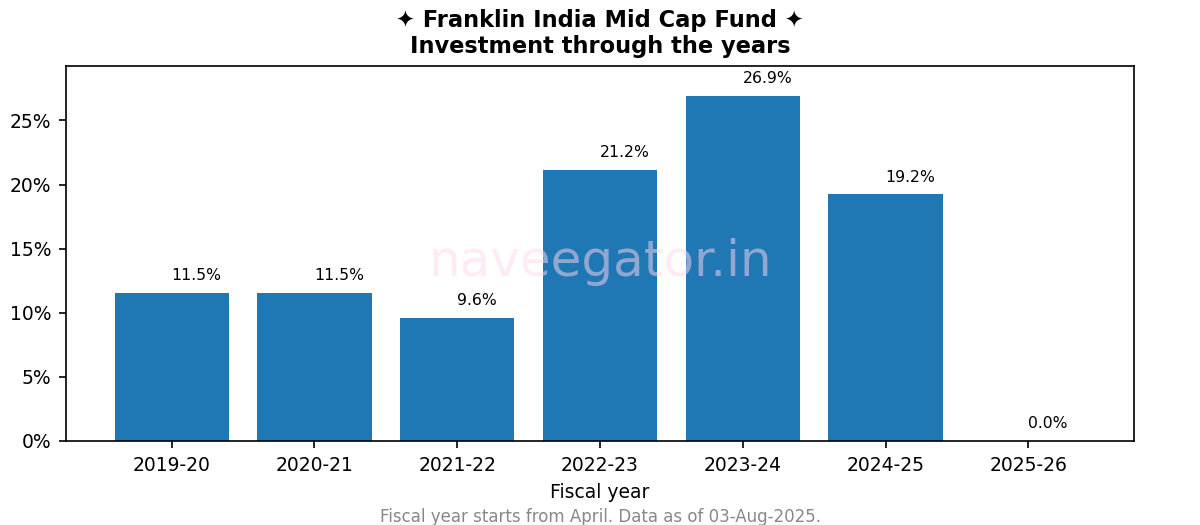

Franklin India Mid Cap Fund continues to underperform Nifty Midcap 50 although over the last 1½ years the gap has reduced a bit (Figure 2). The Trump tariffs are very much visible in the Figure 2. A steep drop in profit starting from Jan’25 and then recovery starting from Mar’25.

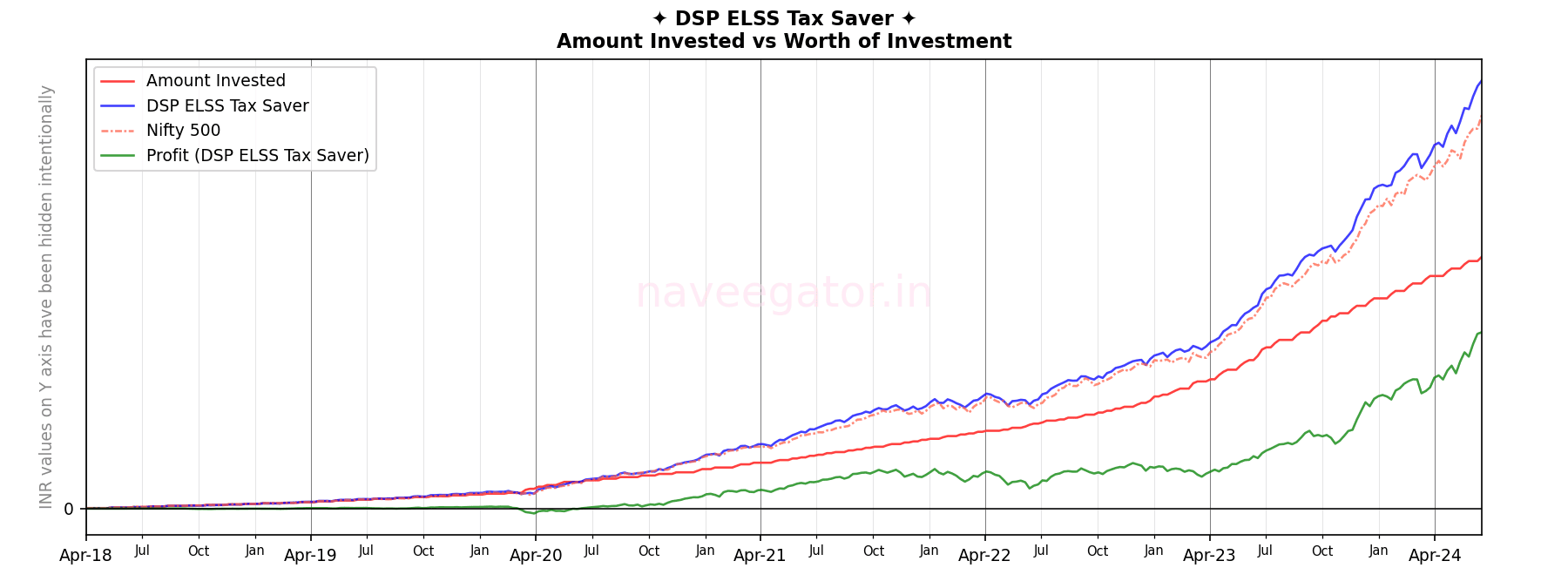

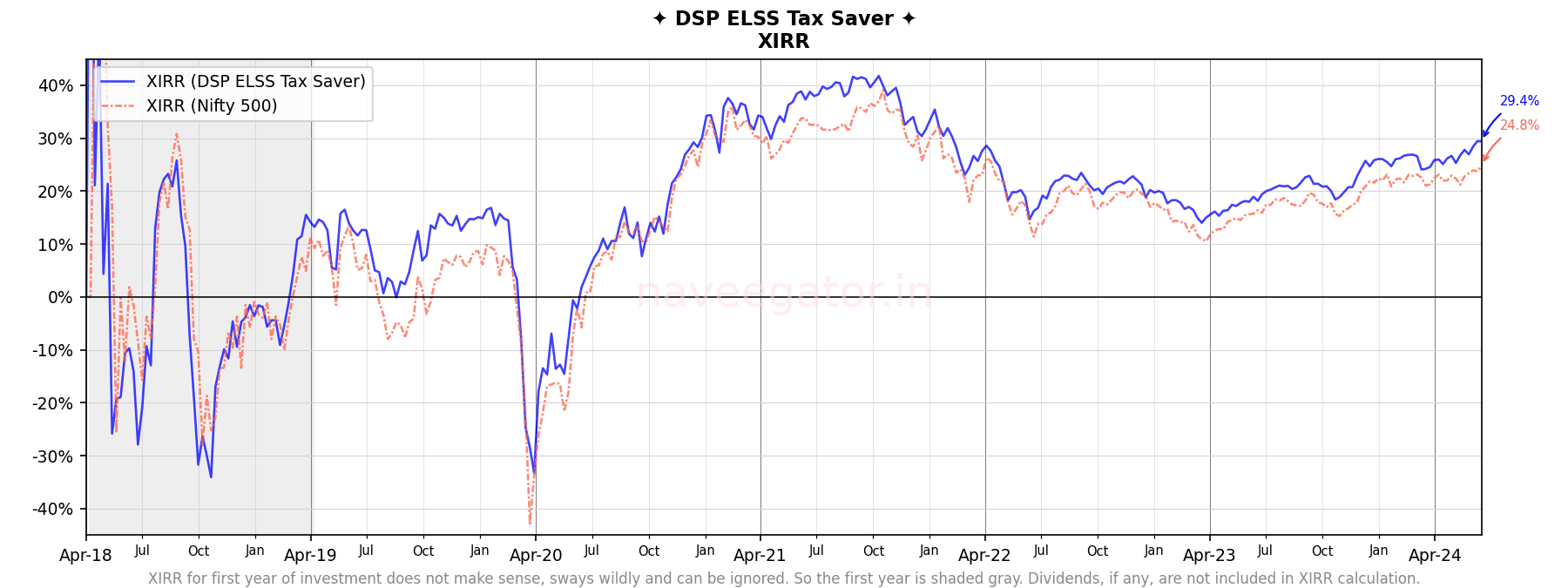

My investment in DSP ELSS Tax Saver started as a way for me to save tax. When I started, I had selected two funds for my ELSS investments, the other one being L&T Tax Advantage Fund. Back then the conventional wisdom to save tax was to invest in ELSS rather than PPF for 80C. Especially if you are young and have a long road ahead of you.

I went via the SIP route and my initial three SIPs were in regular plan. After reading a bit more, learning about direct plans and their lower expense ratios I paused the regular plan SIP and moved to a direct plan.

During my initial years the SIP amount was very low. You can see in Figure 1 that the total investment I made in DSP ELSS Tax Saver Fund during FY 2018-19 is just 2.2% of my overall investments. But as I was tracking the performance of DSP ELSS Tax Saver, I realised the fund was significantly outperforming my other investments—both equity and mutual funds. This prompted me to steadily increase my investments year or year. Come every April and I would increased my SIP amount. The percentage didn’t matter. I increased to whatever I thought I could manage for the next one year. I also sprinkled lump sum investments in between my SIPs—sometimes because I had surplus money to invest, others when the markets were in a tizzy due to some or the other global events.

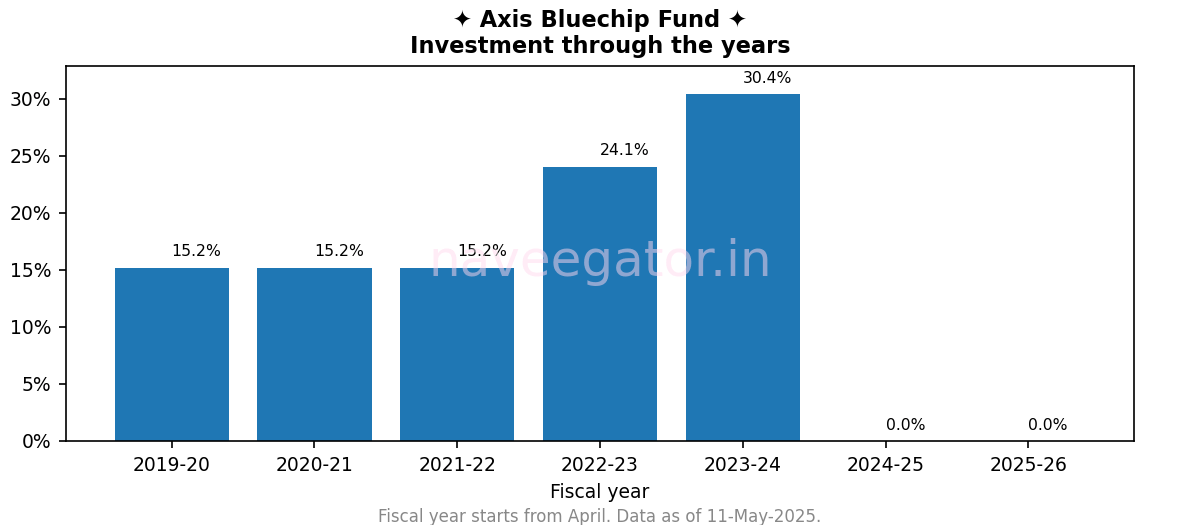

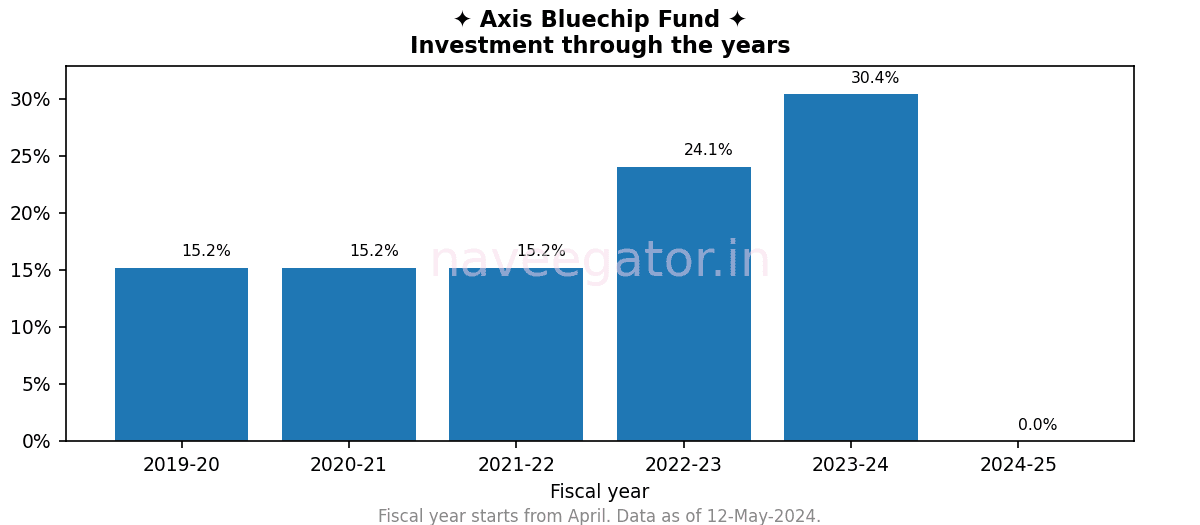

Back in 2019, at my previous workplace, we had a bit of a tradition. Every month or so, stalls would pop up, selling everything from clothes to toys and other knick-knacks. During one of those fairs, I connected with a mutual fund advisor and struck up a conversation about investing. He recommended three funds, one of which was the Axis Bluechip Fund. Since I was investing through an advisor, it would be a regular plan.

Now, I was fully aware of the higher expense ratio that comes with a regular plan. But given that my earlier picks—HSBC ELSS Tax Saver Fund (erstwhile L&T Tax Advantage Fund) and Motilal Oswal Long Term Equity Fund—hadn’t quite met my expectations, I figured it was worth getting some professional help this time. As you read along and see the performance of Axis Bluechip Fund, you will realise that getting professional help, hasn’t helped much. And this is not to put shade on my mutual fund advisor. It is just that some events—as you will read later—are really beyond anyone’s control.

I have stayed with Axis Bluechip Fund for five years starting FY 2019-20. In Sep’22, I decided to increase my SIP. However, this time, I opted for the direct plan to reduce the expense ratio. As a result, this analysis includes investments made through both the regular and direct plans. You can see the uptick in my investments since FY 2022-23 in Figure 1.

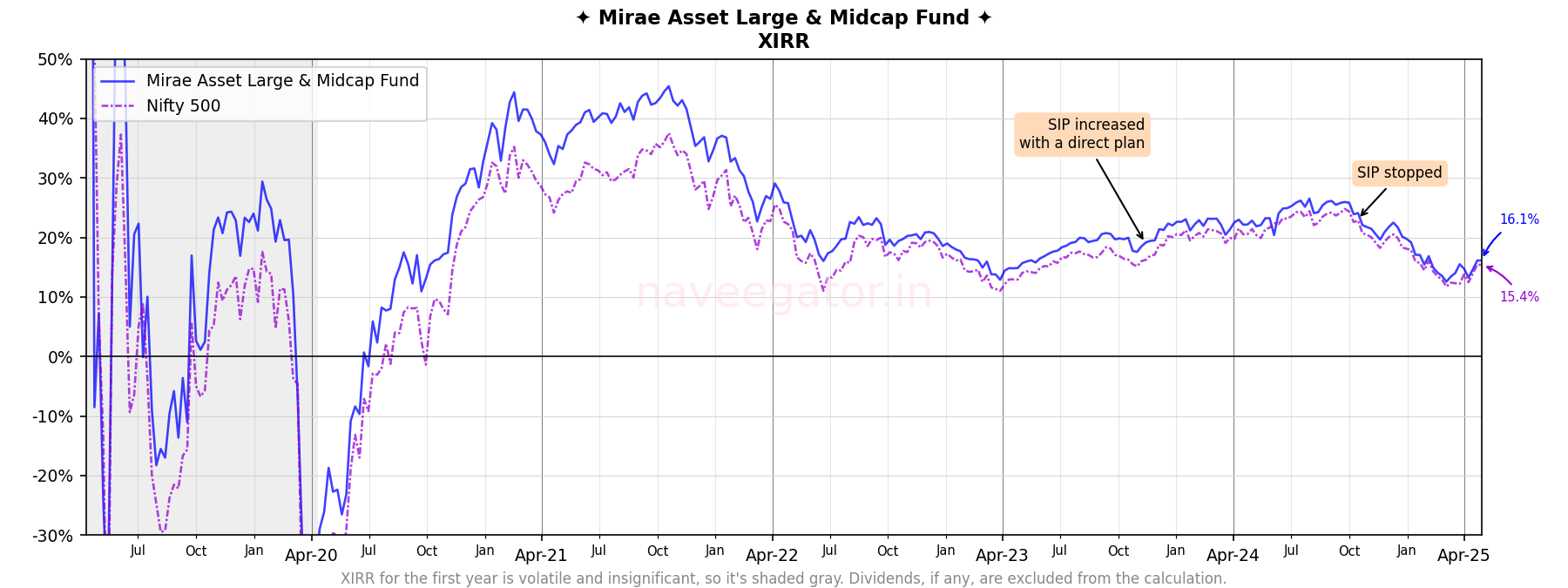

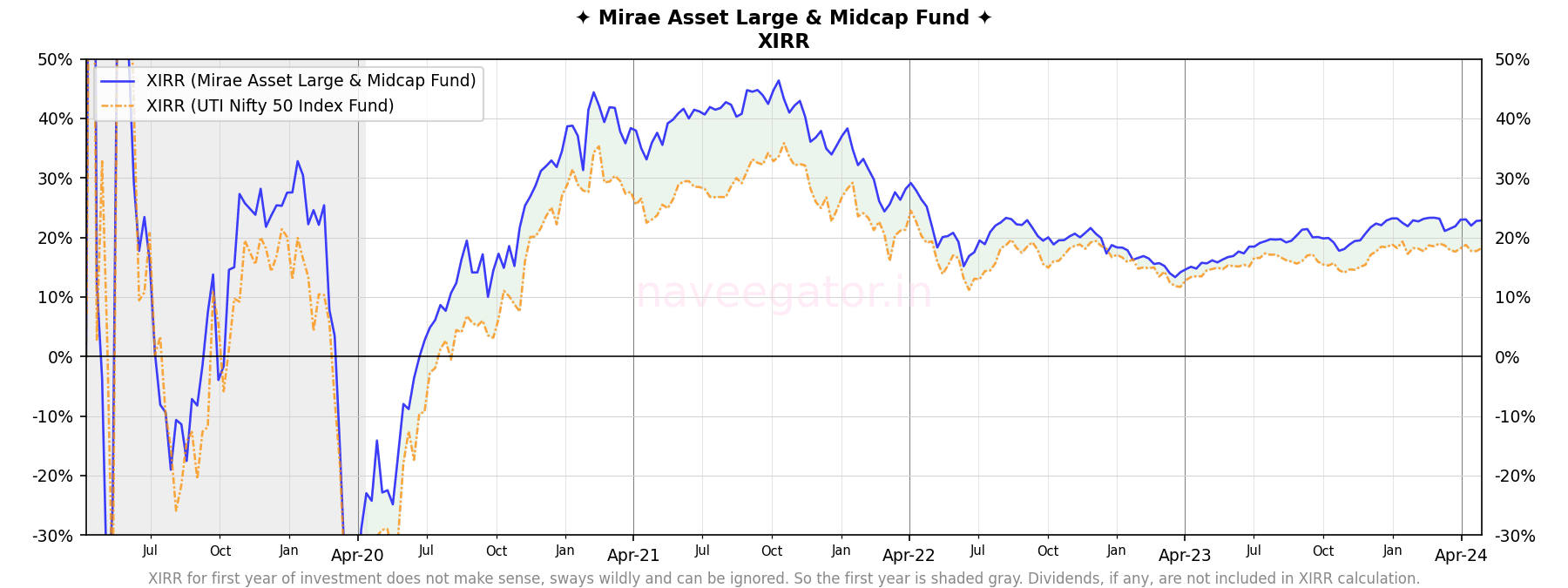

Back in 2018, at my previous workplace, we had a bit of a tradition. Every month or so, stalls would pop up, selling everything from clothes to toys and other knick-knacks. During one of those fairs, I connected with a mutual fund advisor and struck up a conversation about investing. He recommended three funds, one of which was the Mirae Asset Emerging Bluechip Fund. Since I was investing through an advisor, it would be a regular plan.

Now, I was fully aware of the higher expense ratio that comes with a regular plan. But given that my earlier picks—HSBC ELSS Tax Saver Fund (erstwhile L&T Tax Advantage Fund) and Motilal Oswal Long Term Equity Fund—hadn’t quite met my expectations, I figured it was worth getting some professional help this time.

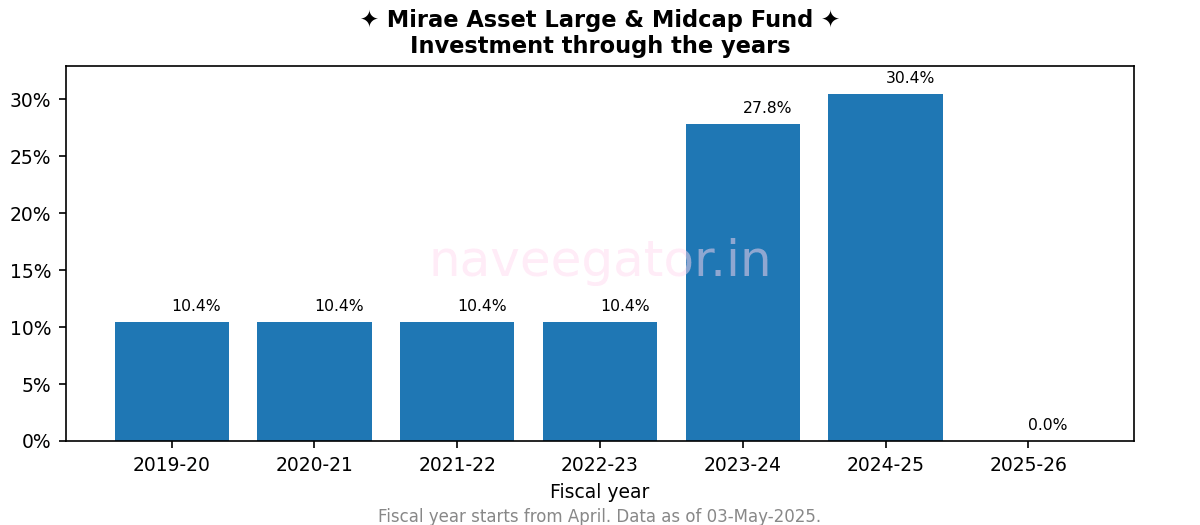

As the months went by and I saw how this fund was performing, I wanted to increase my SIP amount. However, Mirae Asset had placed inflow restrictions on the fund due to its rapid growth and rising AUM. So, I continued with the original SIP amount.

In Oct’23, when Mirae Asset increased the SIP cap, I didn’t waste time. I started a new SIP in the direct plan to benefit from the lower expense ratio, while continuing the old SIP in the regular plan. That’s why you’ll see a noticeable increase in my investment from FY 2023–24 (see Figure 1). Just a month later, in Nov’23, the fund was renamed to Mirae Asset Large & Midcap Fund.

Figure 1

By Nov’24, I paused both SIPs—regular and direct—as I’d invested in a home to diversify my investments and needed capital for the same.

Figure 2

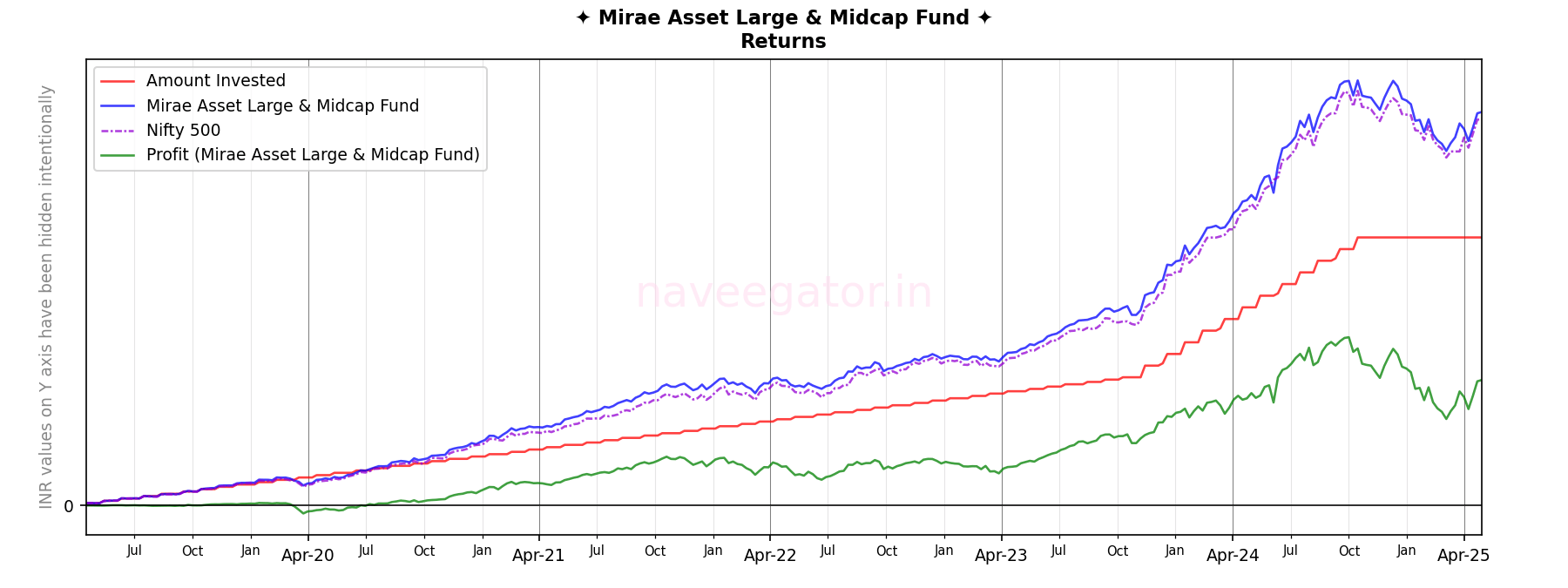

The fund’s benchmark is the Nifty Large Midcap 250 TRI. But since I couldn’t find clean, consistent data for it, I chose to compare the fund’s performance against the Nifty 500 Index instead. Over the years, the fund has consistently outperformed the Nifty 500 (see Figure 3).

Figure 3

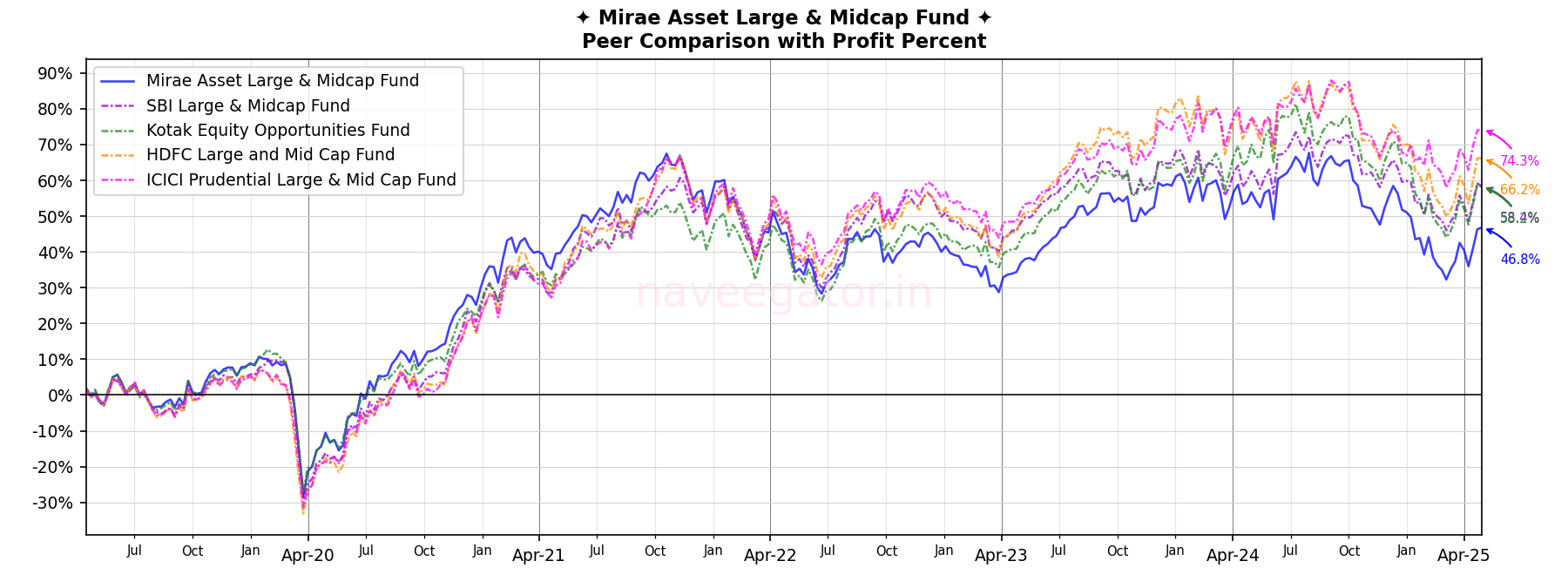

While this comparison looks impressive, things change when I compare the Mirae Asset Large & Midcap Fund with its peers. I’ve compared it with the following direct plans, and Figure 4 shows the profit percentage for each:

SBI Large & Midcap Fund

Kotak Equity Opportunities Fund

HDFC Large and Mid Cap Fund

ICICI Prudential Large & Mid Cap Fund

Figure 4

Mirae Asset’s fund was a top performer until Oct’21. But since then, its performance has deteriorated, and it’s currently the lowest among its peers.

Still, I’m hopeful that in the coming years, the Mirae Asset Large & Midcap Fund will recover and close the gap in performance.

Five years ago I decided to start investing in mid cap mutual fund. There were quite a few of them available for me to choose. Thus, I employed a complex pseudo-random selection algorithm, predominantly utilized by juveniles who, in a display of basic decision-making, chant a seemingly nonsensical yet rhythmically precise incantation. This chant, rich in assonance and consonance, serves as a pretext for arbitrarily designating a mutual fund as the best one, and is often accompanied by the unspoken implication that the outcome is somehow imbued with a semblance of extensive research, despite the process being fundamentally whimsical and capricious.

My algorithm pointed to Franklin India Prima Fund which was one of the oldest with the fund starting way back in 1993. Initially I used to invest only lumpsum amount as when I had surplus. But starting Aug-2021 I decided to start an SIP in the fund. During the market crash of COVID-19, I continuously invested in the fund accumulating units at a lower price.

While the XIRR of 32% appears impressive, a comparison with the Nifty Midcap 50 returns reveals that the fund has consistently underperformed since I began investing in it.

Investment through the years

Returns

Profit

XIRR

How does Franklin India Prima Fund stack up against its competitors?

In the above sections I have demonstrated my investment pattern in the Franklin India Prima Fund and compared its performance against the Nifty Midcap 50 over a period of 5 years. But how does it fare against its competitors? Let’s find out.

I analysed CRISIL’s Mutual Fund Ranking and compared my returns to each of the mid-cap mutual funds. Here’s how I conducted my calculations:

I included only those funds that were established before my first investment in the Franklin India Prima Fund. Therefore, you won’t find fund ITI Mid Cap Fund in the list, as it was launched after my first investment in the Franklin India Prima Fund.

For the competitor funds, I used the same investment amount and dates as those for my investment in Franklin India Prima Fund. This approach allowed me to answer the question, “What if I had invested in ABC Midcap Fund?”

The table below illustrates the profit percentages I would have earned from the Franklin India Prima Fund and its competitors. It’s clear that I would have been significantly better off investing in the Motilal Oswal Midcap Fund. However, this doesn’t capture the journey each fund took to reach their current positions.

Fund

Profit Percent (as of 01-Aug-2024)

CRISIL MF Ranking (as of 30-Jun-2024)

Aditya Birla Sun Life Midcap Fund

89.9%

4

Axis Midcap Fund

82.8%

3

Baroda BNP Paribas Mid Cap Fund

99.1%

3

DSP Midcap Fund

79.1%

5

Edelweiss Mid Cap Fund

116.7%

2

Franklin India Prima Fund

93.4%

3

HDFC Mid-Cap Opportunities Fund

111.7%

2

HSBC Mid Cap Fund

98.8%

3

ICICI Prudential MidCap Fund

100.5%

2

Invesco India Mid Cap Fund

101.4%

3

Kotak Emerging Equity Fund

103.7%

3

LIC MF Midcap Fund

94.4%

2

Mahindra Manulife Mid Cap Fund

118.3%

1

Motilal Oswal Midcap Fund

136.9%

1

Nippon India Growth Fund

113.5%

2

PGIM India Midcap Opportunities Fund

88.8%

5

SBI Magnum Midcap Fund

95.8%

3

Sundaram Mid Cap

99.9%

3

Tata Mid Cap Growth Fund

100.5%

3

UTI Mid Cap Fund

91.5%

4

The below line chart demonstrates the performance of various mid cap mutual funds over the past five years. Notably, the PGIM India Midcap Opportunities Fund outperformed all other mid cap funds—that too by a significant margin—until April 2023. However, the fund’s performance has declined since then.

Another effective way to analyze mid cap mutual fund performance is through a bar chart race. The below visualization highlights the dominance of the PGIM India Midcap Opportunities Fund until April 2023. Since then, several other funds have overtaken it. As for the Franklin India Prima Fund, it has consistently ranked among the bottom five!

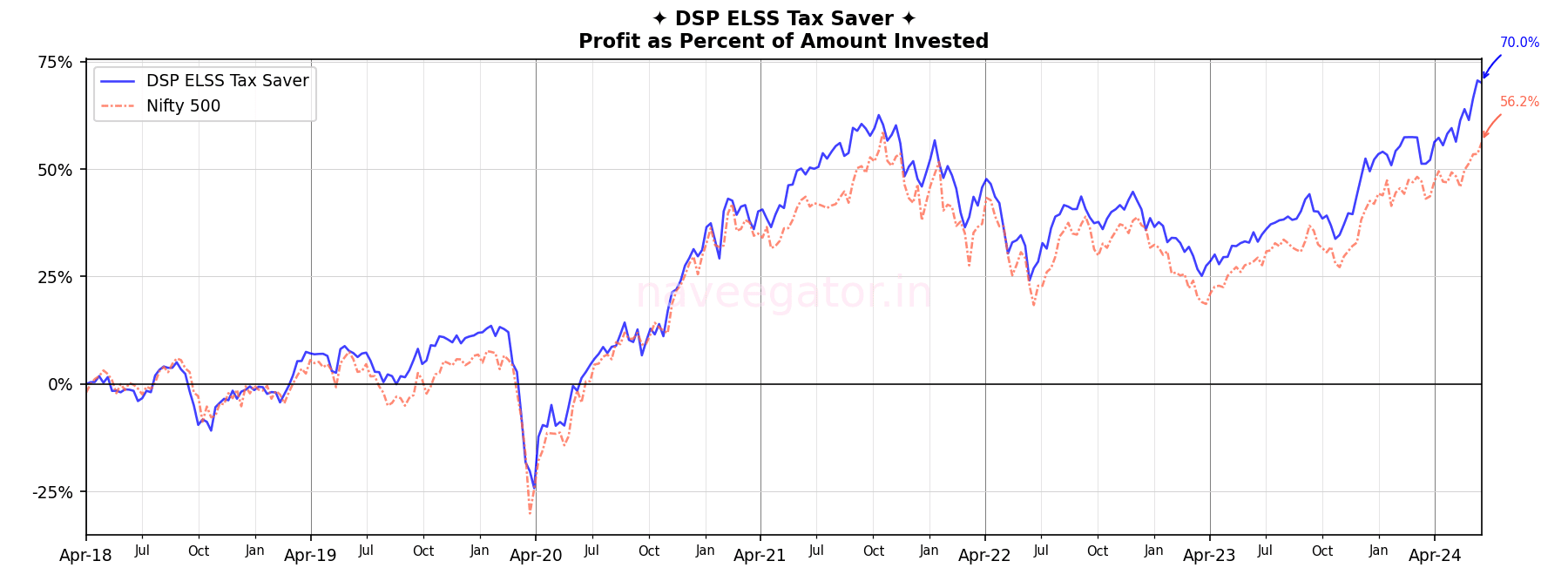

My investment in DSP Tax Saver started as a tool for saving taxes. After government announced new income tax regime, I knew that the tax benefits of Section 80C would soon go away. I was about to pause my investments in DSP Tax Saver but looking at its performance I did not. Looking back, I’m happy with that I decided to continue.

For me, the fund has been outperforming its benchmark—Nifty 500—since the last 3 years; something which my other funds have struggled to do consistently. And due to its continued outperformance I have been increasing my SIPs every year in this fund.

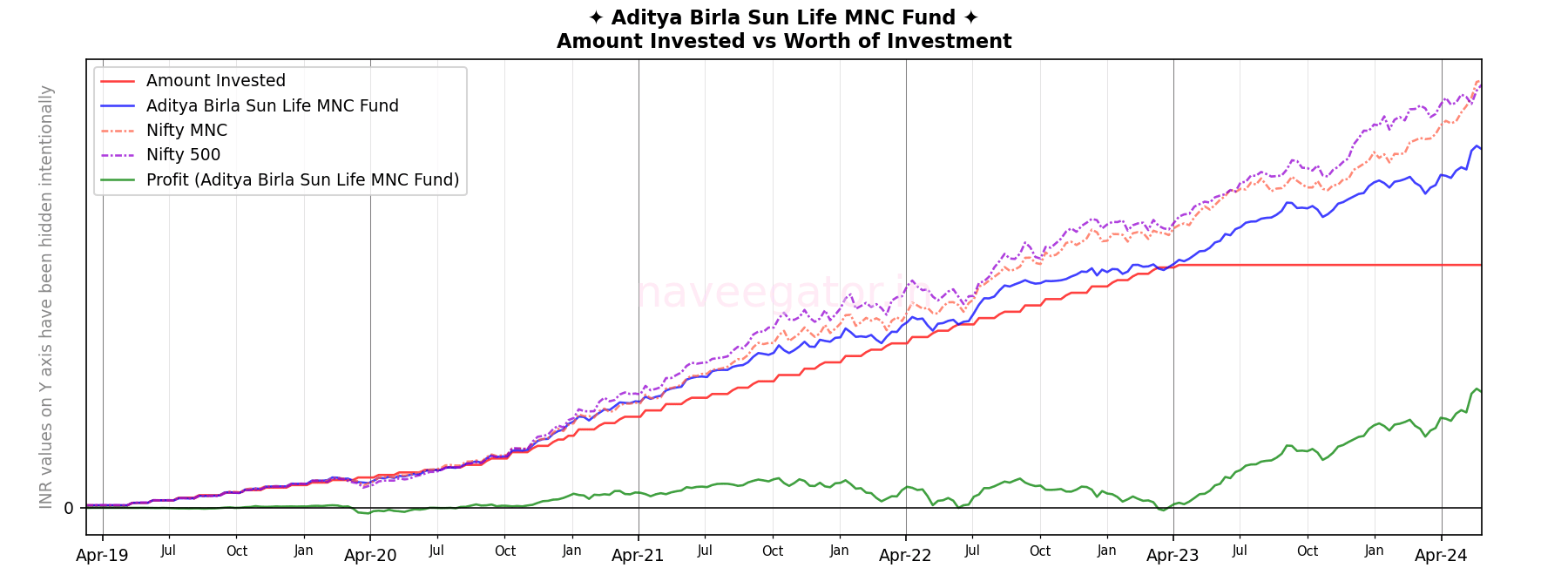

I started investing in Aditya Birla Sun Life MNC fund after consulting my mutual fund advisor in March 2019. The initial years of investment were quite impressive, yielding good returns and boosting my confidence in this particular fund. This positive performance prompted me to initiate another SIP via the direct route, hoping to maximize my gains.

However, things took a turn for the worse starting in October 2021. The fund began to underperform consistently. I monitored the fund’s performance closely, hoping for a recovery, but the disappointing trend persisted. This underperformance led me to rethink my investment strategy.

In April 2023, I decided to pause my SIP in the Aditya Birla Sun Life MNC fund. Consequently, I shifted my money to other funds that were performing reasonably well, such as the DSP Tax Saver Fund. This fund had shown consistent performance over a period, which made it a more attractive option for my investment portfolio.

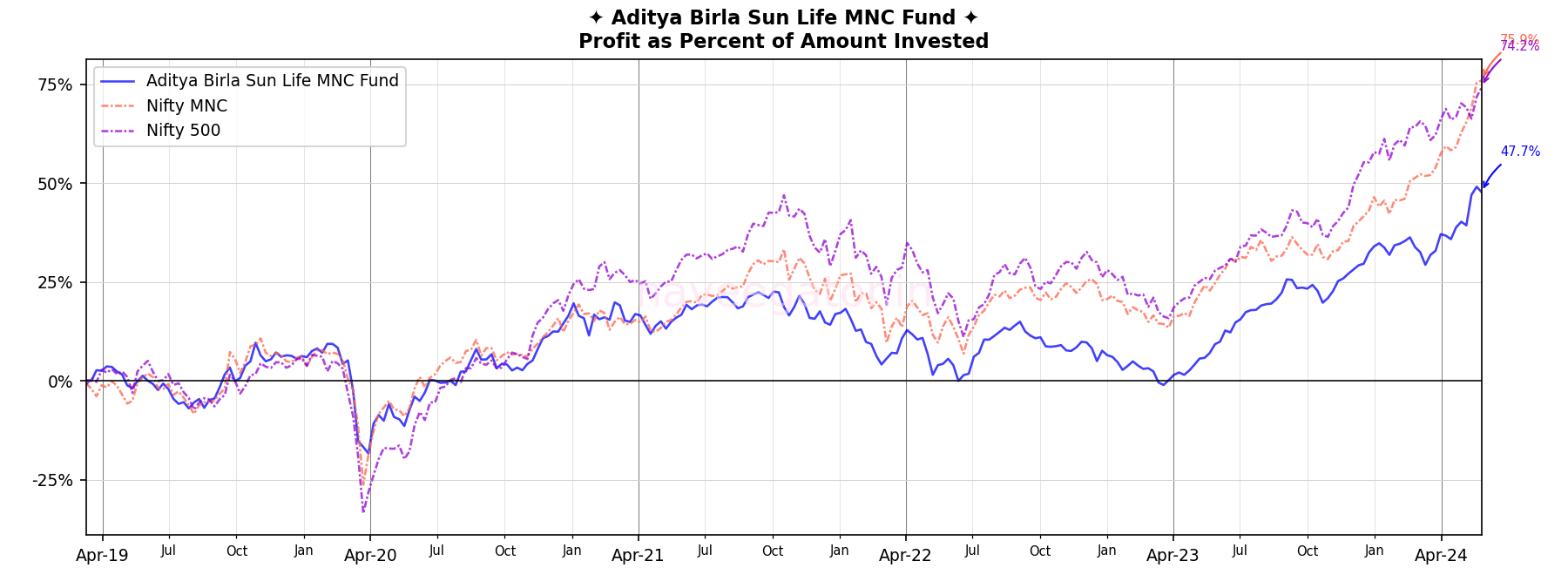

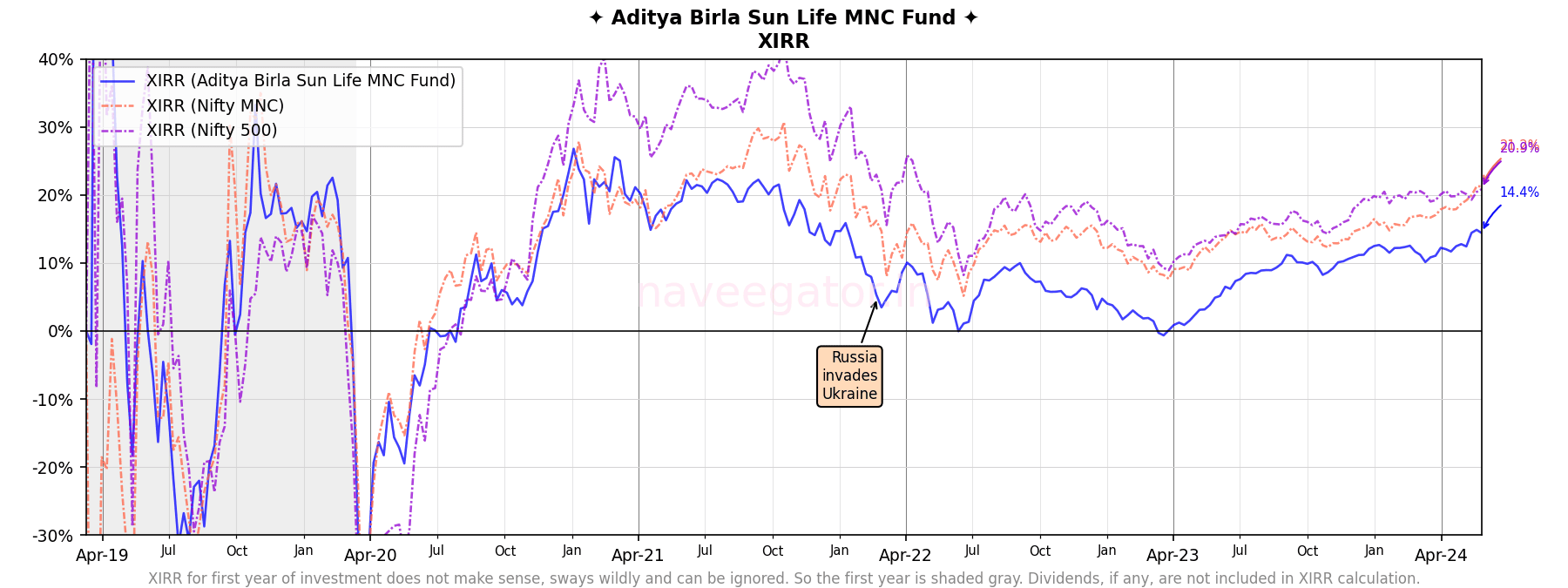

Since last one year the fund performance has improved significantly. Get this, Apr 2023 my XIRR was 0% and Apr 2024 my XIRR is 14%.

With this improvement in performance, the fund has closed the gap against its benchmark, the Nifty MNC index, which shows that the strategies implemented might be aligning well with market trends. However, while the gap has been reduced, the fund still lags behind the Nifty MNC index.

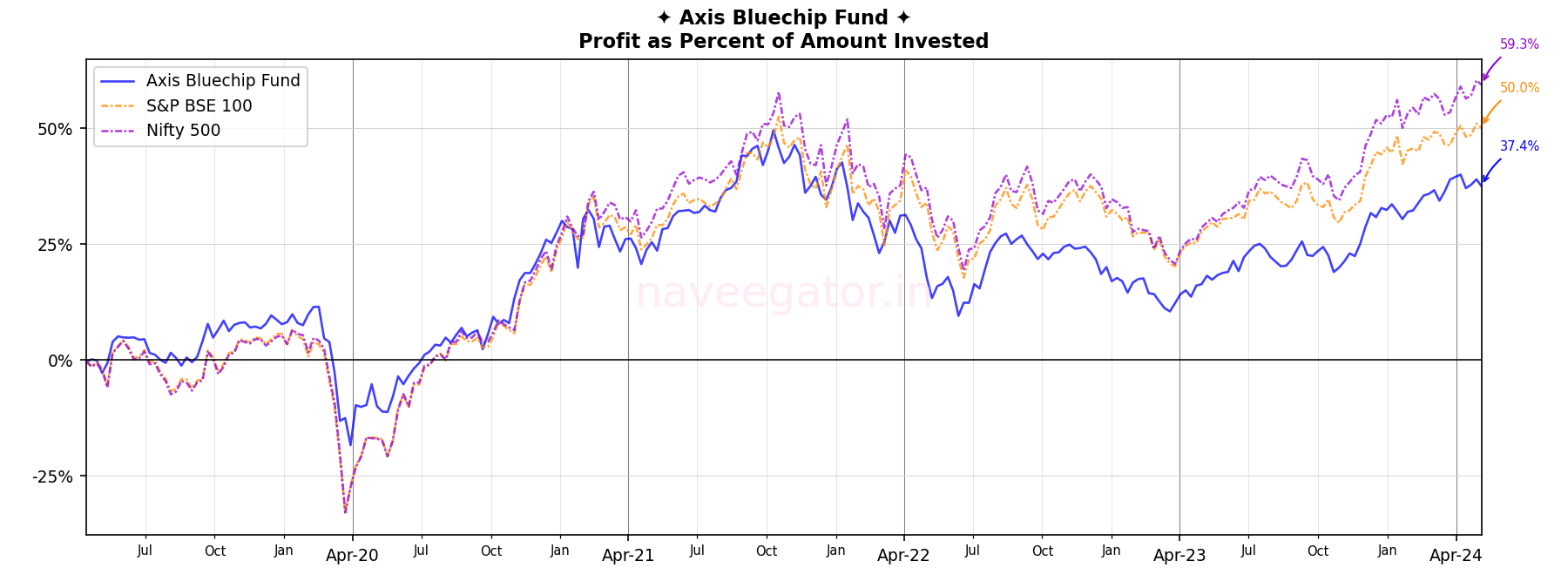

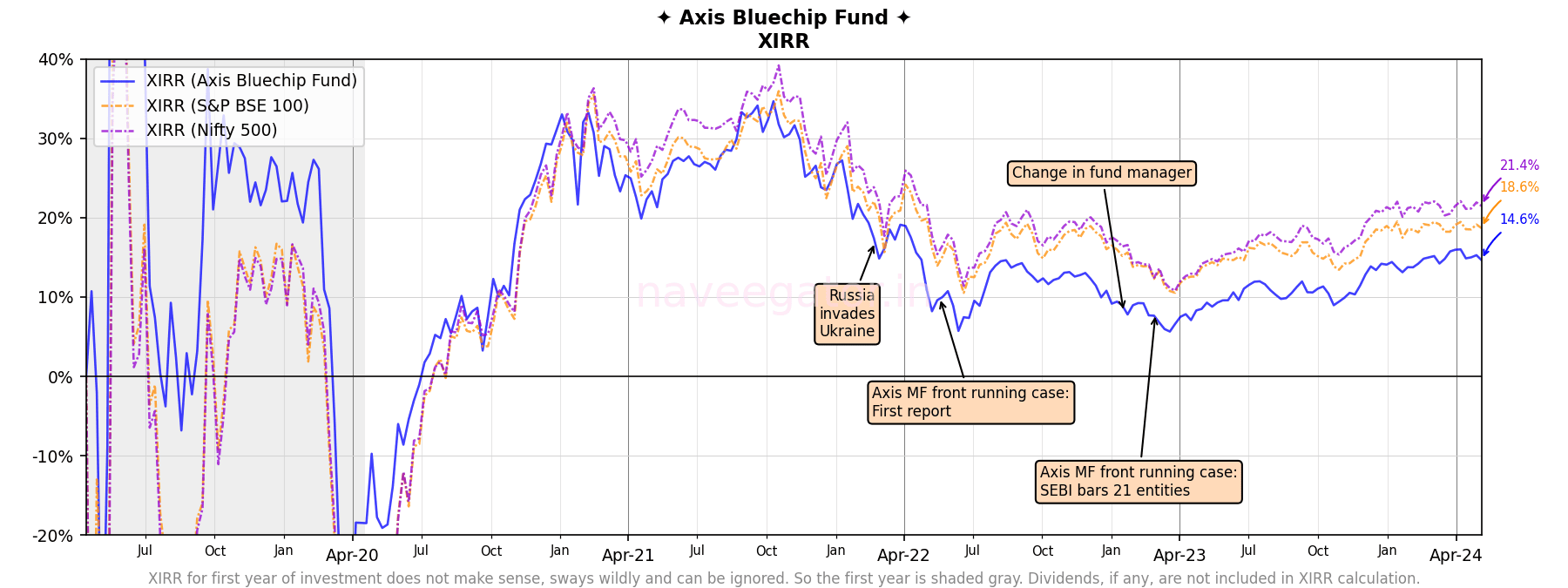

My journey with Axis Bluechip Fund completed five years and it was the year where I decided to call it a pause on the investment. Its continued underperformance against its benchmark S&P BSE 100 was the primary reason to take a pause. And to some extent the Axis front running case was also responsible for my decision.

Is this a regular or a direct plan? It’s both. I started with a regular plan with help of MFD and then from Sep-2022 I started investing in the direct plan as well. The charts below are for both of them combined. Regular plan holds 76% of my investment while the direct plan holds the remaining 24%.

Did I beat the benchmark S&P BSE 100? No. Since last three years, my investment has underperformed the S&P BSE 100.

Am I going to continue investing in it? No, I am pausing further investments.

My investment in DSP Tax Saver started as a tool for saving taxes. After government announced new income tax regime, I knew that the tax benefits of Section 80C would soon go away. I was about to pause my investments in DSP Tax Saver but looking at its performance I did not. And, at least as of now, I am glad that I did not.

Is this a regular or a direct plan? I started off with a regular plan but after three SIP instalments, I learned about direct plan and switched to it. Only 1% on my investment in DSP Tax Saver is in regular plan and while rest 99% is in direct plan. So it is safe to say this is a direct plan.

Did I beat the Nifty 50 Index? Yes, but by a small margin. While Nifty 50 Index would have given 16% XIR, DSP Tax Saver has given me 18%.

How does my return compare to other ELSS mutual funds? I decided to compare my returns to the top ELSS fund as per CRISIL’s Mutual Fund Ranking dated 31-Mar-2023 i.e. Quant Tax Plan. Compared to Quant Tax Plan my investment in DSP Tax Saver has underperformed, and that too by a huge margin. Quant Tax Plan’s XIRR comes at 30% compared to DSP Tax Saver’s 18%.

So, will I move to Quant Tax Plan? No.

Am I going to continue investing in DSP Tax Saver? Yes, at least for another year.

You must be logged in to post a comment.