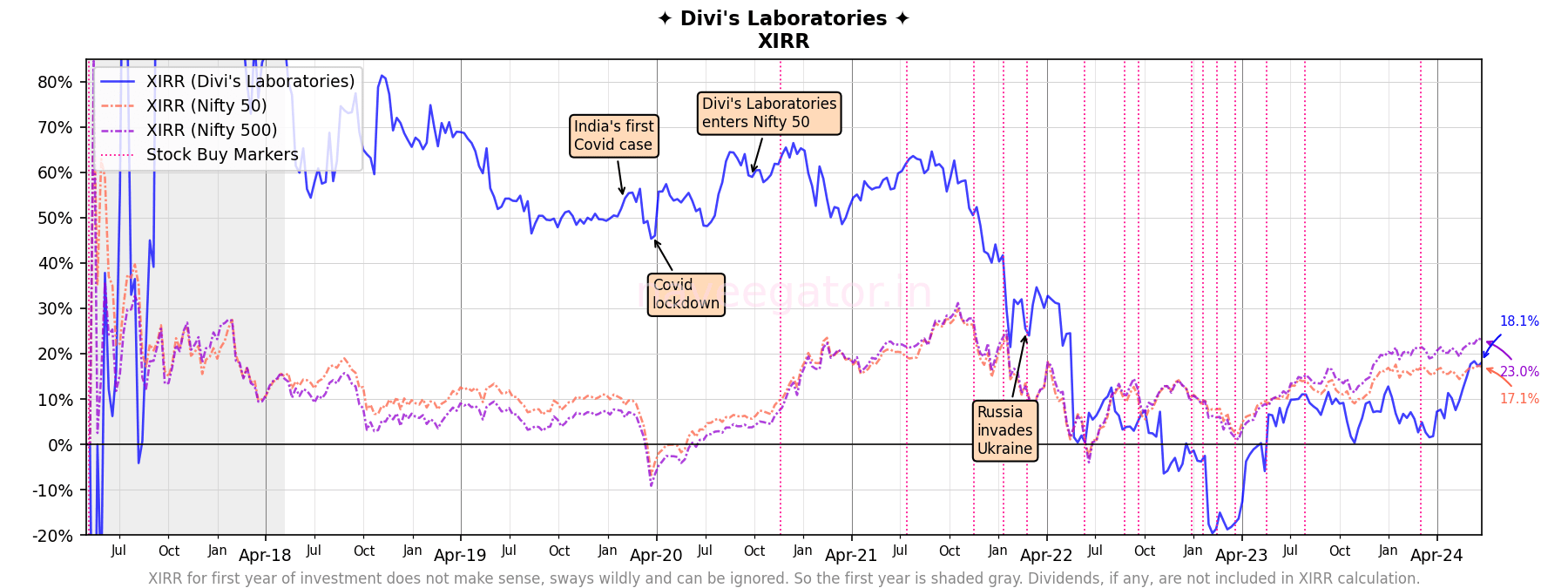

My investment in Divi’s Laboratories has been my biggest missed opportunity. Six years back—still new to equity investing—I was looking for Pharma stocks to invest. During that research—not sure if I should call it research, but let’s go with it—I came across Divi’s Laboratories. I made a small investment in it and forgot about it. In the next 3.5 years the stock went up 5 times! And I did not make a single new investment during that time! Every time I thought “it can’t go up any further than that”. Boy was I wrong. So, so wrong!

Since FY 2020-21, I have slowly started increasing my investments in Divi’s Laboratories. But the stock—on the other hand—has been volatile. During April’23 the stock went on a downward spiral and my XIRR went to -20%. What happened at that time? Finshots has an explanation for that.

Over the last fiscal year Divi’s Laboratories has slowly recovered and is now beating Nifty 50 by a razor thin margin. Yay! Hopefully this recovery continues.

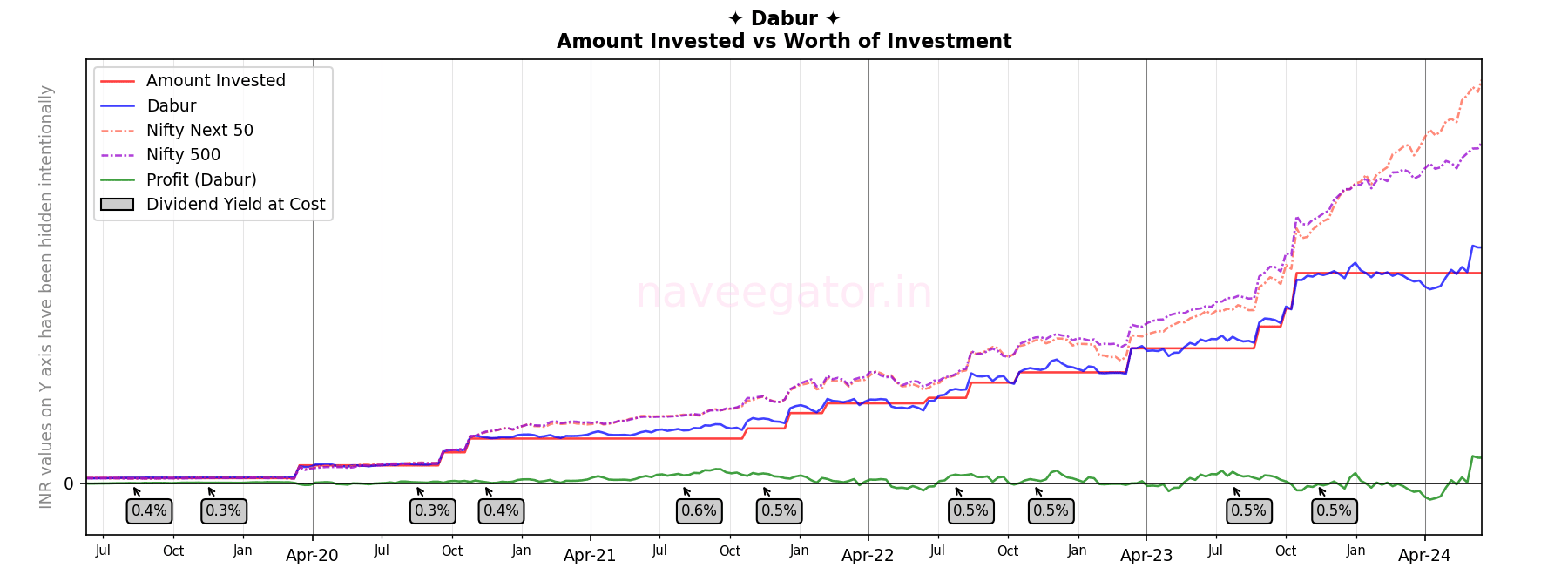

Over the last five years I have steadily increased by investment in Dabur. The stock—on the other hand—has gone sideways, zig-zagging between positive and negative sides of zero; never truly rising up and—thankfully—never crashing drastically.

There is really nothing to write about here apart from my anxiety about holding a stock for long term.

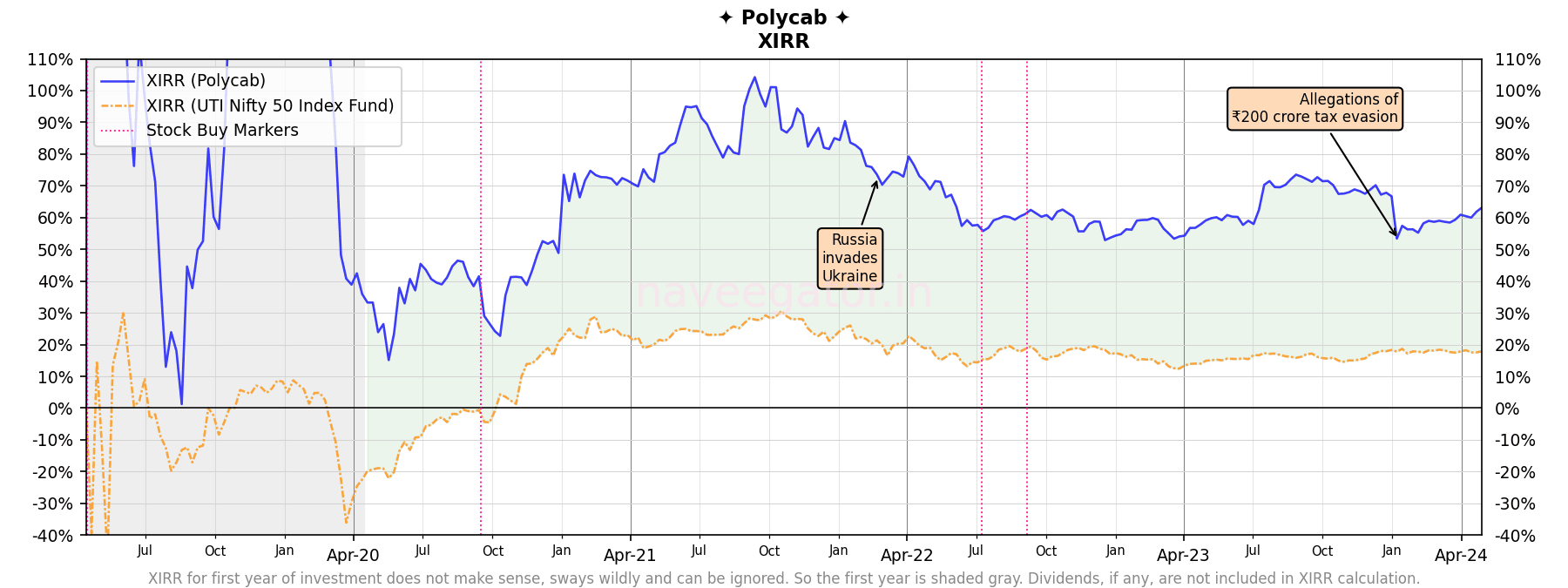

In 2024, my investment in Polycab took me on a roller coaster ride. Early in the year, allegations of ₹200 crore tax evasion were leveled against the company. As a result, the stock plummeted from ₹5,400 to ₹3,800. I felt like my golden goose was dying. My profit dropped from 500% to 325%, which, while still impressive, felt disappointing compared to the initial gains. Unsure whether the allegations were true, I grappled with the decision: should I sell Polycab and secure a gain of over 300%? Ultimately, I chose to do… nothing. I sat there, eyes closed, waiting. Remarkably, four months later, Polycab has fully recovered its lost gains. But the mystery remains: were the allegations true or false? And what happens if they are true?

Investment through the years

Returns

Fiscal year

Dividend yield at cost

2019-20

1.86%

2020-21

0.00%

2021-22

1.45%

2022-23

1.27%

2023-24

2.13%

2024-25

0.00% *

* Data as of 4-May-2024

The dividend yield at cost mentioned in the Returns graph above, is yield at the date at which I received the dividends. Another way to look at dividend yield is to calculate it for the fiscal year. To calculate the dividend yield at cost in the above table I use the below formula. (Total amount of dividends received in a fiscal year ÷ Total amount invested at the end of fiscal year) × 100

Seven years ago when I started investing in Samvardhana Motherson International Ltd, it was called Motherson Sumi Systems Limited. Over last seven years the company split its wiring business into another entity called Motherson Sumi Wiring India Limited and renamed itself to Samvardhana Motherson International Ltd.

When Motherson Sumi Wiring Ltd got demerged, the historical share price of Samvardhana Motherson International Ltd got adjusted to remove Motherson Sumi Wiring Ltd’s valuation (not sure if I am using the right terminology here, I am no financial expert). With that I was not able to reliably calculate the historical movement of my investment. But this time, I used the technique described here with the difference being that I used Google Sheets rather than Numbers on Mac.

Before we go see the journey, here is gist of the key events.

Date

Event

Jul 2017 from Motherson Sumi Systems Ltd

Bonus 1:2

Oct 2018 from Motherson Sumi Systems Ltd

Bonus 1:2

Feb 2022

Motherson Sumi Wiring Ltd demerges with 1:1 ratio i.e. one equity share of Motherson Sumi Wiring Ltd for every one equity share of Motherson Sumi Systems Limited

Sep 2022 from Motherson Sumi Wiring Ltd

Bonus 2:5

Sep 2022

Motherson Sumi Systems Limited renames itself to Samvardhana Motherson International Ltd

Oct 2022 from Samvardhana Motherson International Ltd

Bonus 1:2

Investment through the years

I have not invested any amount since I last wrote, so the my investment through the years looks the same as last years.

Returns

Returns and Profit Percent chart were created using Google Sheets so it would look different from my other articles. Also, you would notice that the comparison with Nifty 50 Index is also missing; I am yet to figure that out. One thing to note here is that, last year has been good for both Samvardhana Motherson International and Motherson Sumi Wiring India.

Profit Percent

Looking at profit percent, it becomes even clearer how good last year has been. Till last year I was at loss of 2.5% while this time around I am at profit of 62%!

XIRR

I cannot create XIRR chart in Google Sheet. So you will have to read the words here.

My XIRR now is at 9.5%. If I compare it to XIRR of Nifty 50 Index it would have been 15%. Although I am still behind Nifty 50 Index returns, but I think there may be a point in time in the future where my investment will beat the Nifty 50 Index. This was unimaginable for me till last year.

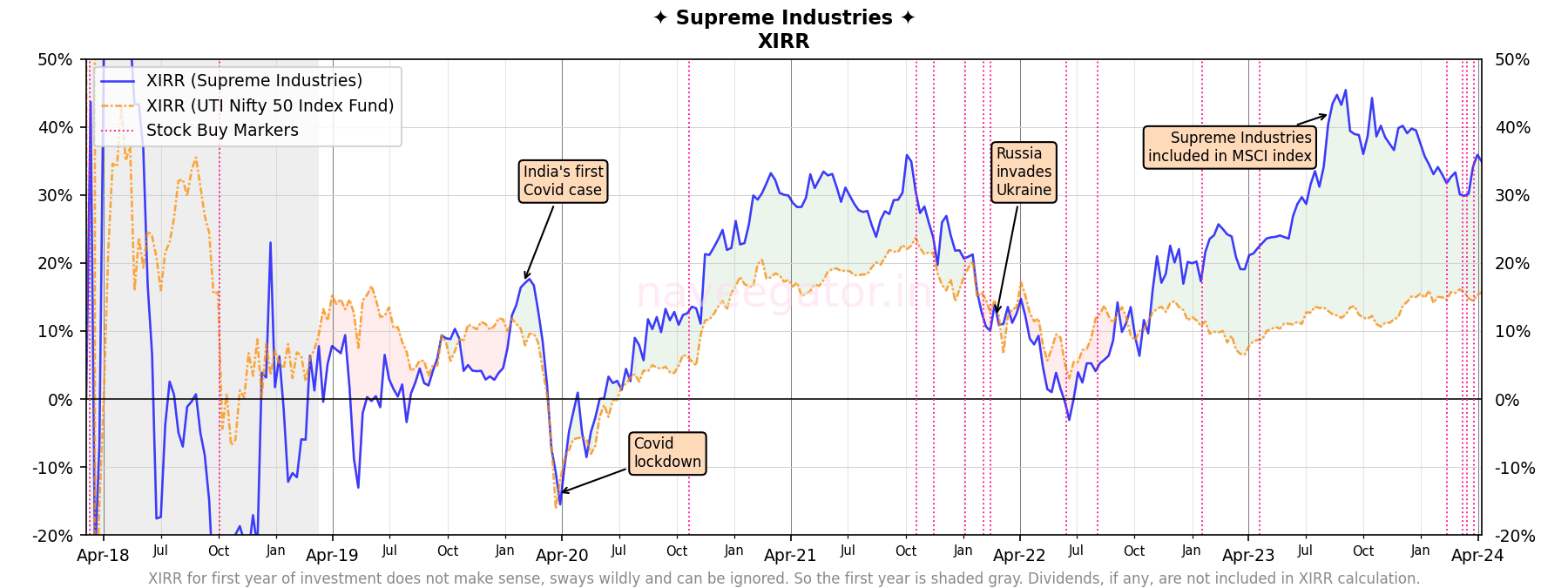

As the last fiscal year (2023-24) unfolded, Supreme Industries witnessed remarkable growth in its share price. Getting included in MSCI index also helped the growth. As a result at one point, my XIRR soared to an impressive 45%!

There was a minor correction, causing the stock price to dip below ₹4000. Undeterred by the temporary setback, I seized the opportunity to accumulate more shares, capitalizing on the lower price. Fast forward to the present—57% of my investment poured in during the last fiscal year (2023-24) alone! Interestingly, this situation mirrors the previous year where—at that time—three quarters of my investment came in last two fiscal years.

Investment through the years

Returns

A dividend yield at cost of 1% is… good enough.

Fiscal year

Dividend yield at cost

2018-19

0.75%

2019-20

2.14%

2020-21

0.42%

2021-22

0.65%

2022-23

1.13%

2023-24

1.02% *

* Data as of 9-Apr-2024

The dividend yield at cost mentioned in the Returns graph above, is yield at the date at which I received the dividends. Another way to look at dividend yield is to calculate it for the fiscal year. To calculate the dividend yield at cost in the above table I use the below formula. (Total amount of dividends received in a fiscal year ÷ Total amount invested at the end of fiscal year) × 100

Profit

XIRR

A remarkable 35% XIRR, compared to the Nifty 50 index’s 15%, is truly impressive! Now, the question remains: How long will it maintain this remarkable performance?

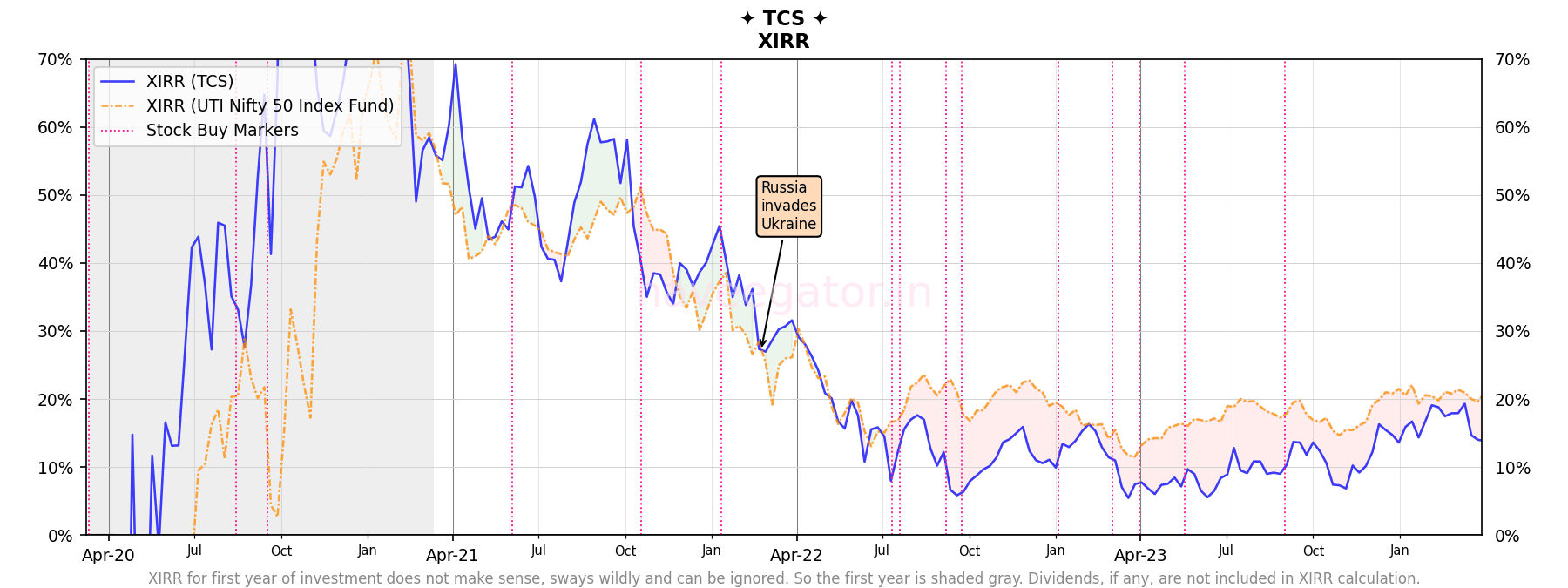

I cannot get around that no matter what I do, beating the market consistently is very hard, and even if I manage it, it is more due to luck than skill. I am no longer excited whenever I see a new tweet, article, or video about a new product.

The idea of passive or index investing has killed my passion for investing.

After two years of underperforming the Nifty 50, the above statement rings true for me. And if it happens with a company as solid as TCS, then I think I am also better off with investing in Nifty 50 index.

Investment through the years

Four years is a less of a timeframe for equity investments and when 65% of those investments have come in last two years, I need to be patient. Maybe in next four years things will be different.

Returns

TCS has been good with dividends. 2%+ dividend yield at cost is something that would consider good.

The dividend yield at cost mentioned in the chart above, is yield at the date at which I received the dividends. Another way to look at dividend yield is to calculate it for the fiscal year.

Fiscal year

Dividend yield at cost

2019-20

0.61%

2020-21

0.93%

2021-22

1.07%

2022-23

2.91%

2023-24

2.11%

To calculate the dividend yield at cost in the above table I use the below formula.

(Total amount of dividends received in a fiscal year ÷ Total amount invested at the end of fiscal year) × 100

Profit

XIRR

14% XIRR should sound good, right? But when you see 20% XIRR on the Nifty 50 index it… pinches!

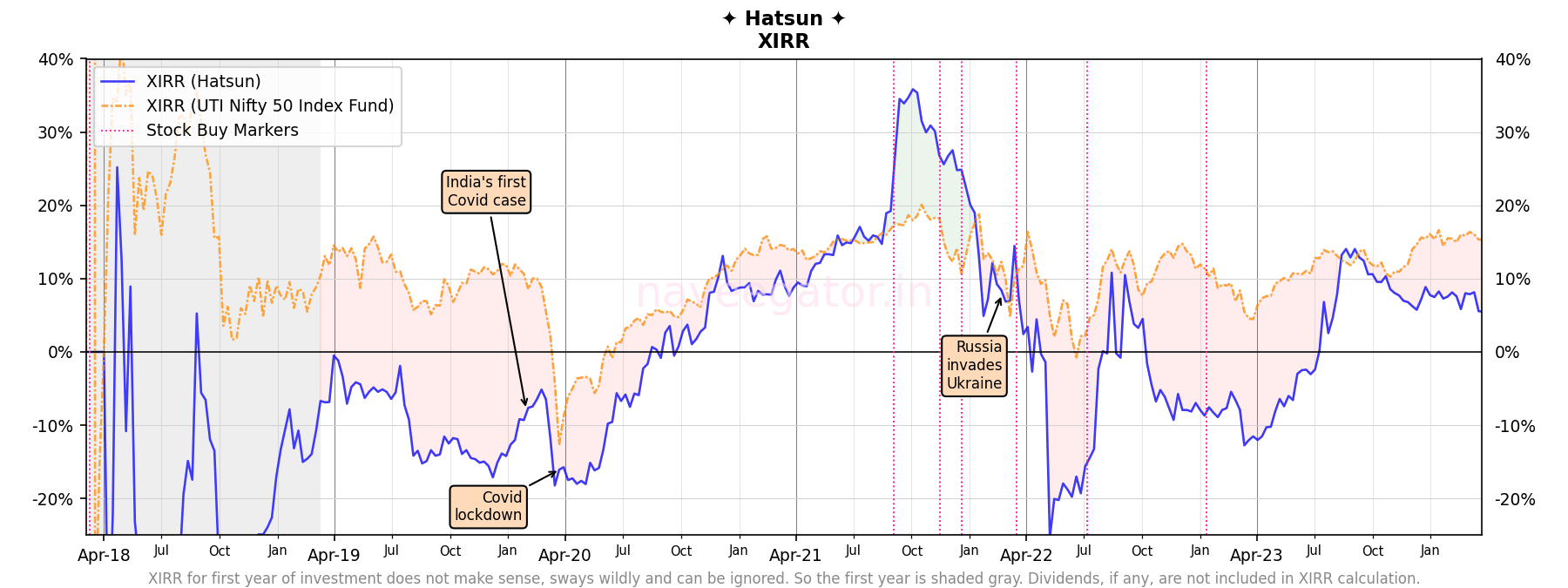

I am not quite sure why I am writing this post on my shareholding journey of Hatsun when I have more or less given up on the company. I am planning to exit Hatsun once I see a brief uptick where it at least goes over 10% XIRR. With underperformance spanning over five years, all that is stopping me from selling off is that my 90%+ investment in Hatsun has come in the last 3 years.

Let’s see if I am blogging about my journey next year.

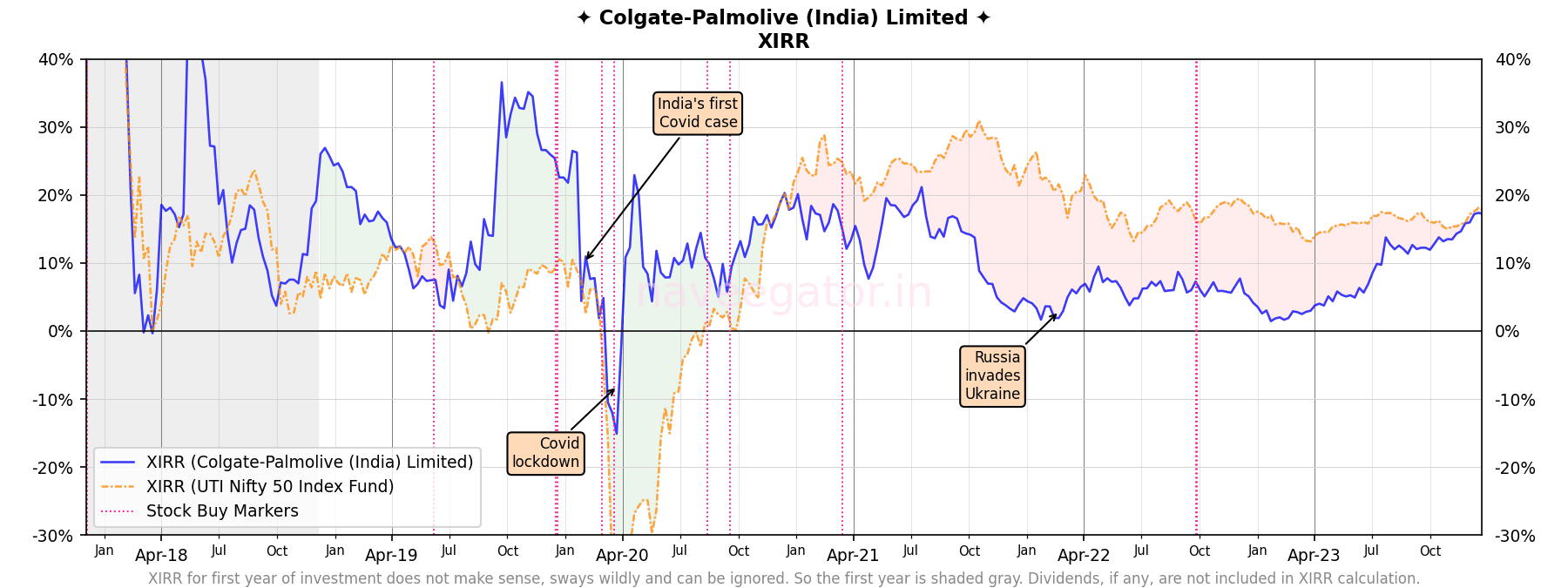

Continuing my investment in Colgate—which has been underperforming since 2 years—has been a very painful experience. I still have my conviction on this stock after five years, albeit it is now on shaky ground.

My conviction has paid off this year. From the beginning of the year, Colgate has experienced a steady upward trend, with a remarkable increase of over 65%. Following three years of lagging behind the Nifty 50 Index, my investment in Colgate has now successfully bridged the gap. Given the current momentum, I am confident that it will outperform the Nifty 50 Index in the coming year. Additionally, the dividends have proven to be satisfactory.

Investment through the years

Returns

The dividend yield at cost mentioned in the chart above, is yield at the date at which I received the dividends. Another way to look at dividend yield is to calculate it for the fiscal year.

Fiscal year

Dividend yield at cost

2017-18

0.87%

2018-19

1.83%

2019-20

0.59%

2020-21

3.31%

2021-22

1.40%

2022-23

2.51%

2023-24

3.07% *

* Data as of 28-Dec-2023

To calculate the dividend yield at cost in the above table I use the below formula.

(Total amount of dividends received in a fiscal year ÷ Total amount invested at the end of fiscal year) × 100

Profit

XIRR

Related reading

Note: I missed including some of my Colgate-Palmolive (India) Limited share purchases in previous articles. These are rectified in this post, so there will be difference between my previous analysis and this one.

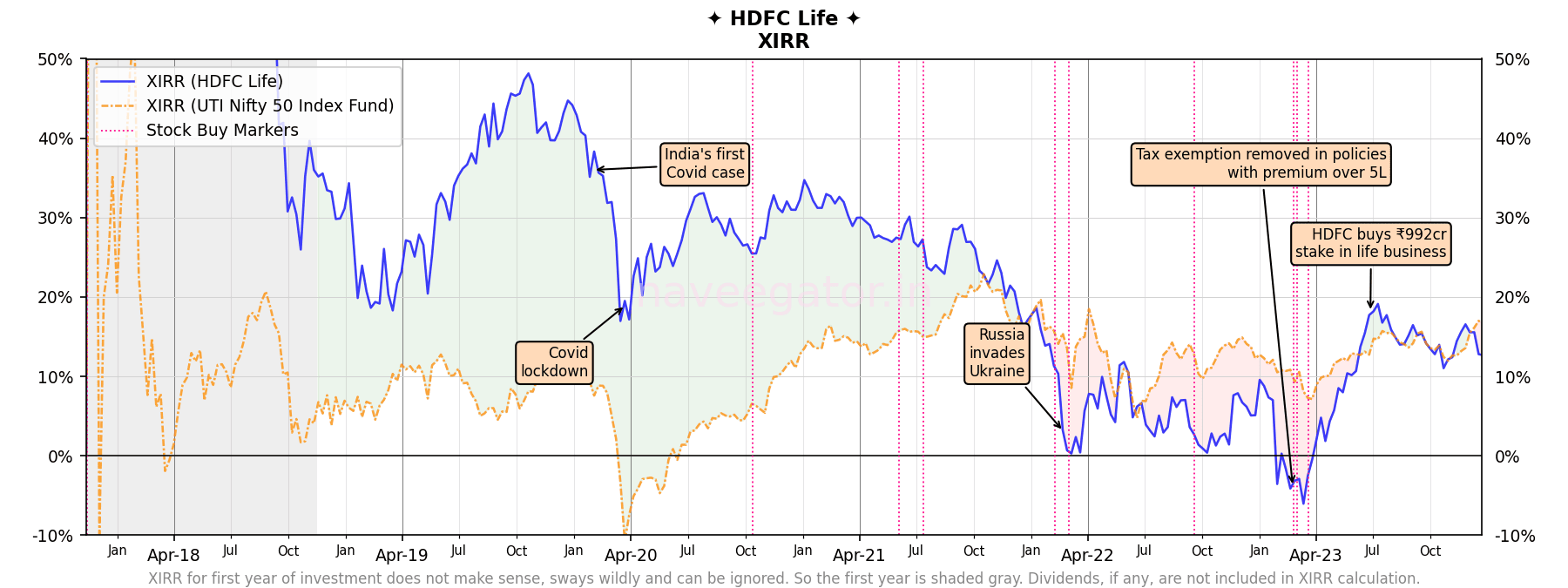

Six years ago I subscribed to the HDFC Life Insurance IPO. And I got lucky! HDFC Life Insurance opened up with a nice 17% gain on first day. I sat on my luck for few years not investing much agin. It was only in the FY 2021-22 and 2022-23 that I significantly increased my allocation. In fact 88% of my investment in HDFC Life Insurance has come in last two and half years, so my investment is still very young.

Tax tweak in life insurance

This was a significant announcement in the Budget 2023.

Income from traditional insurance policies where the premium is over Rs 5 lakh will no more be exempt from taxes, Finance Minister Nirmala Sitharaman announced in her Budget speech.

And this change would impact profitability of almost all the life insurance products.

The changes to tax exemption on life insurance policies announced by Finance Minister Nirmala Sitharaman in her 2023 Budget speech on February 1 are likely to have a 10-12 percent impact on the topline products of HDFC Life and a 5 percent impact on the bottomline products if nothing is done to mitigate the change, predicts Vibha Padalkar, MD and CEO of HDFC Life Insurance.

And with that announcement my returns—for the first time in 5 years—became negative. I used that opportunity to invest more. In the hindsight—I think—it was a good decision. The share price has recovered and I am at 12% XIRR. Although I am still underperforming Nifty 50 Index where I would have made 16%.

Investment through the years

Returns

The dividend yield at cost mentioned in the chart above, is yield at the date at which I received the dividends. Another way to look at dividend yield is to calculate it for the fiscal year.

Fiscal year

Dividend yield at cost

2017-18

0.47%

2018-19

0.57%

2019-20

0.00%

2020-21

0.00%

2021-22

0.17%

2022-23

0.17%

2023-24

0.38% *

* Data as of 24-Dec-2023

To calculate the dividend yield at cost in the above table I use the below formula.

(Total amount of dividends received in a fiscal year ÷ Total amount invested at the end of fiscal year) × 100

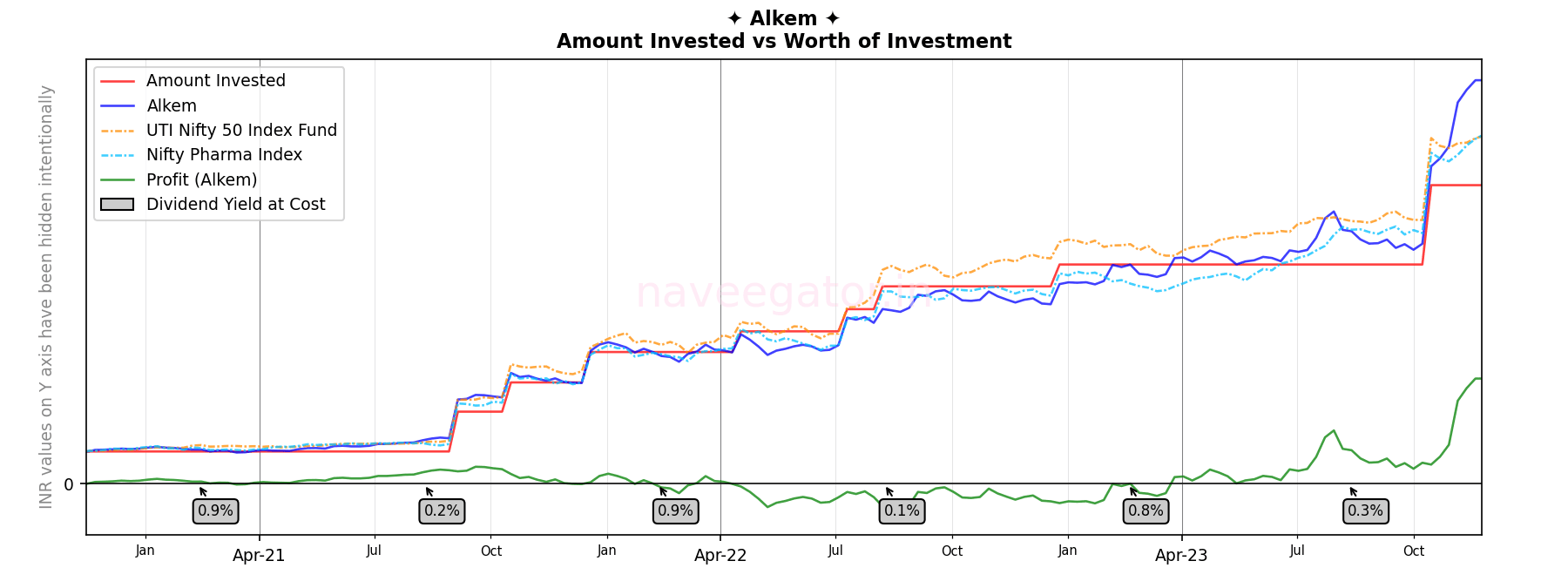

Three years ago, I made the decision to invest in Alkem solely based on its inclusion in the Nifty Next 50 index. Without conducting any further research or analysis, I relied on the belief that companies included in Nifty Next 50 index are generally considered to be well-established and stable. What I didn’t consider was that Alkem can also be removed from the Nifty Next 50 index.

Alkem is now no longer part of Nifty Next 50 index and its underperformance vis-a-vis Nifty 50 index since last two years had made my palms sweaty. But there has been a very recent uptick in the share price where it has gone up by almost 25% in last one month. While I would have made 10% XIRR with Nifty 50 Index I am now at 22% XIRR with Alkem. Let’s see how long the party lasts.

Investment through the years

Returns

The dividend yield at cost mentioned in the chart above, is yield at the date at which I received the dividends. Another way to look at dividend yield is to calculate it for the fiscal year.

Fiscal year

Dividend yield at cost

2020-21

0.92%

2021-22

0.92%

2022-23

0.87%

2023-24

0.22% *

* Data as of 26-Nov-2023

To calculate the dividend yield at cost in the above table I use the below formula.

(Total amount of dividends received in a fiscal year ÷ Total amount invested at the end of fiscal year) × 100

![Seven years as shareholder of Samvardhana Motherson International Ltd [and Motherson Sumi Wiring India Ltd]](https://naveegator.in/wp-content/uploads/2024/05/Motherson_Apr24_AmountINvested.png)

{kind=link}